|

Debt Bombs: Here Are The States With The Most Debt

ZeroHedge.com Sat, 09/28/2019 - 22:00 According to a new report from Truth in Accounting, the most-indebted states include New Jersey, Illinois, Connecticut, Massachusetts, Hawaii, Delaware, Kentucky, California, and New York. Truth in Accounting published the Financial State of the States report, a regional analysis of the most recent state government financial data, on Tuesday, that is one of the most comprehensive studies of the economic conditions of all 50 states. The report includes the most up-to-date state finance and pension data, trends across the states, and key findings. The report said all 50 states have had to become more transparent in their financial reporting over the last several years, thanks to the implementation of Generally Accepted Accounting Principles set by the Governmental Accounting Standards Board. Researchers this year uncovered something truly shocking: "40 states do not have enough money to pay all of their bills and in total the states have racked up $1.5 trillion in unfunded state debt." Truth in Accounting ranks the states below according to their Taxpayer Burden or Surplus, which at the end of the day, it's what the taxpayer is on the hook for. Here are the rankings (from less indebted to most indebted):

One user said: "Look at who has controlled the State Legislatures in all the high debt States - in nearly every case it has been the Democrats, and for many years. Governors come and go - it is the Legislature that really decides if a State will be wild spending or not." Another said: "I live in Illinois. Lifelong Illinoisan. Yes I know it sucks. My 5 year plan is to leave the state before it collapses financially any home value plummets. Property taxes, sales taxes and income taxes are insane over here. DO NOT MOVE HERE." The biggest take away from the report, as explained by one social media user above, is that when the next recession strikes, the most indebted states will collapse. https://www.zerohedge.com/personal-finance/debt-bombs-here-are-states-most-debt

0 Comments

Got Gold? In Search Of The 'Effective' Lower Bound

by Tyler Durden Thu, 09/26/2019 - 14:37 Authored by Mike Shedlock via MishTalk, The Fed is no longer talking about zero-bound but effective lower bound. What's the difference? Where is it? The self-described "BondFreak" noticed a shift in Fed vocabulary from "zero bound" to "effective lower bound". Why? Powell Ready to Cut Rates to "Effective Lower Bound" via "Conventional" Policy A Google search for "effective lower bound" just happened to turn up my own post Powell Ready to Cut Rates to "Effective Lower Bound" via "Conventional" Policy. Here are the pertinent statements from a speech Powell made on June 4 at a "Conference on Monetary Policy Strategy, Tools, and Communications Practices". Emphasis is mine. While central banks face a challenging environment today, those challenges are not entirely new. In fact, in 1999 the Federal Reserve System hosted a conference titled "Monetary Policy in a Low Inflation Environment." Conference participants discussed new challenges that were emerging after the then-recent victory over the Great Inflation. They focused on many questions posed by low inflation and, in particular, on what unconventional tools a central bank might use to support the economy if interest rates fell to what we now call the effective lower bound (ELB). Even though the Bank of Japan was grappling with the ELB as the conference met, the issue seemed remote for the United States. The next time policy rates hit the ELB—and there will be a next time—it will not be a surprise. We are now well aware of the challenges the ELB presents, and we have the painful experience of the Global Financial Crisis and its aftermath to guide us. Our obligation to the public we serve is to take those measures now that will put us in the best position deal with our next encounter with the ELB. The big difference between then and now is that the federal funds rate was 5.2 percent—which, to underscore the point, put the rate 20 quarter-point rate cuts away from the ELB. Since then, standard estimates of the longer-run normal or neutral rate of interest have declined between 2 and 3 percentage points, and some argue that the effective decline is even larger. The combination of lower real interest rates and low inflation translates into lower nominal rates and a much higher likelihood that rates will fall to the ELB in a downturn. Why the shift? I believe the answer is the Fed no longer believes zero is the ELB. So this leads to a different question. Where the Heck is the ELB? First, we need a definition. What's the Definition of ELB? Effective Lower Bound is the point beyond which further monetary policy in the same direction is counterproductive. I propose the Bank of Japan and the ECB are already below ELB. I further propose the ELB can never be negative but it can be well above zero. Reversal Interest Rate I happened across an article just the other day on the ELB moving target. Please consider The Reversal Interest Rate The “reversal interest rate” is the rate at which accommodative monetary policy “reverses” its intended effect and becomes contractionary for the economy. It occurs when recapitalization gains from duration mismatch are more than offset by decreases in net interest margins, lowering banks’ net worth and tightening its capital constraint. The determinants of the reversal interest rates are (i) banks asset holdings with fixed (non-floating) interest payments, (ii) the strength of the constraints that they face, (iii) the degree of interest rate pass-through to deposit rates, and (iv) the initial capitalization of banks. Furthermore, quantitative easing increases the reversal interest rate and hence should only be employed after interest rate cut is exhausted. Over time the reversal interest rate creeps up, since the capital gains effect fades out as longterm bonds holdings mature while the net interest margin effect does not. The authors propose the rate can be above or below zero but it gets higher over time especially if QE is involved. Bank Lending Constraints In our model, as in reality, the risk-taking ability of the banking sector is constrained by its net worth. If the latter is high enough so that the constraint does not bind, or if capital gains are strong enough to actually increase net worth, then an interest cut generates the boom in lending that the central bank seeks to induce. However, if capital gains are too low to compensate the loss in net interest income, net worth decreases to the point where the constraint binds, limiting banks’ ability to take on risk. At that point, i.e. at the reversal interest rate, any further interest cuts generate a decline in lending though the net-worth feedback. Moreover, an interesting amplification mechanism emerges. As the negative wealth effect further tightens banks’ equity constraint, banks cut back on their credit extension and are forced to increase their safe asset holdings. As safe assets yield lower returns, banks’ profits decline even more, forcing banks to substitute out of risky loans into safe assets, which in turn lowers their profit, and so on. Bingo Huge Failure Already I discussed lending constraints the other day (and many time priors) in ECB's New Interest Rate Policy "As Long As It Takes" Huge Failure Already Banks Lend Under Two Conditions

Negative interest rates did not induce either Japanese or European banks to lend. What's Going On? Either European banks are more capital impaired than the ECB wants everyone to believe, or banks believe there are few good credit risks worth taking. Take your pick. I expect both are true. Stealth Recapitalization We then uncover the determinants of the reversal interest rate in our baseline model. The reversal interest rate depends on bank assets interest rate exposure, the tightness of financial regulation, as well as the market structure of the banking sector. If banks hold more longterm bonds and mortgages with fixed interest, the “stealth recapitalization” effect due to an interest rate cut is more pronounced, and the reversal interest rate is lower. Stricter capital requirements rise the reversal interest rate. Lower market power, which decreases profits, also generates a higher reversal interest rate. For example, in a negative interest rate environment, innovations that allow depositors to substitute bank accounts for cash more easily hurt the banks’ margins and raise the reversal interest rate; if such innovation occurs below the reversal interest rate, it directly feeds back into lower lending. The article mentions "stealth recapitalization" of banks. I have discussed that many times recently but in a different context. The Fed pays interest on excess reserves but the ECB charges them. Whereas the Fed gave free money to banks, the ECB charged the banks for excess reserves it forced into the system. Negative Interest Rates Are Social Political Poison In contrast to the authors, I do not believe negative interest rate policy can ever work as it violates basis economic principles on time preference and the time value of money. Moreover, a dive below the ELB supports the position I presented on September 23: Negative Interest Rates Are Social Political Poison ELB Comments

Searching for the ELB is like chasing tails. It's only by accident can a central bank catch the tail. But even if it does catch the tail, the tail can still move. Further efforts to re-catch the tail are as likely as not to be in the wrong direction. With that, let's return to the BondFreak's question. Why the word change? Perhaps the Fed is aware the ECB is on the wrong course, negative rates are counterproductive, or the ELB just might be above zero. Perhaps it's meaningless happenstance. Deeper Down the Rabbit Hold Yesterday, I noted Draghi Open to MMT and a People's QE Every attempt to fix the perceived problem of "too low inflation" goes deeper and deeper down the rabbit hole. It's economic madness, yet, here we are. The solution is to let the free market set interest rates rather than a tail-chasing consortium of economic wizards who have never spotted a bubble or a recession in real time. Of, course, we also need to get rid of central banks and fractional reserve lending. Got Gold? Unfortunately, central banks will not vote to abolish themselves. It's also certain that government efforts to take direct control of money will be even worse than the actions of central banks. A position is gold is the best counter to monetary policy madness. Repo Market Guru: "Whatever Changed Last Week Is Clearly Still A Problem"

by Tyler Durden Thu, 09/26/2019 - 05:11 Last week around this time, most of the self-described repo experts on twitter and elsewhere were pounding the table, screaming to anyone who would listen that the unprecedented spike in overnight general collateral repo from 2.25% to 10% was a non-event, and reflects one-time items such as the mid-September tax remittance, the rapid build up of cash in the Treasury's general account and a flurry of Treasury settlements. Alas, as we warned, and as the NY Fed today confirmed, the sudden heart attack in the critical, overnight funding market has turned out to be anything but a one-time event. First, as we saw first thing this morning, the latest repo overnight repo operation was the most oversubscribed yet, with $91.95BN in securities tendered for $75BN in reserves, the most yet since the Fed resumed these "unclogging" operations after a decade plus hiatus. However, the big surprise came later on Wednesday morning, when in an "unexpected" move, the Federal Reserve expanded the size of its two dollar funding operations, the overnight and term repo, from $75BN to $100Bn, and from $30Bn to $60BN heading into quarter-end, effectively injecting up to $250 billion in funding ($30BN in already concluded term repo as well as two $60BN term repos yet to come, together with the $100BN overnight repo, assuming full allottment on all operations, for a grand total of $250BN). Commenting on this dramatic expansion in Fed liquidity injections, BMO's rates expert ian Lyngen, had a simple, if very powerful observation: "the fact that we’re discussing a quarter trillion dollars is telling as to the depth of the constraint in repo." Indeed a far cry from the "all clear" the twitter repo "experts" were screaming from the top of their lungs last week. As we approach quarter-end, it’s intuitive that funding markets are attracting heightened attention after last week’s repo fiasco. One thing has become clear, however, and that is that the Fed is willing to provide significant amounts of liquidity to primary dealers to alleviate as much stress as possible. By upsizing injections to $250 bn or more (assuming overnight remains at $100 bn through October 1 and the terms are $30 bn/$60 bn/$60 bn, respectively) the fact that we’re discussing a quarter trillion dollars is telling as to the depth of the constraint in repo as well as the New York Fed’s desire to make September 30 boring. At the end of the day, only primary dealers are counterparties of this facility. This presents a possibility of some upward pressure on rates were cash not to have permeated throughout the system by the reporting date. Confirming Lyngen's fears, and in a troubling indication that despite the Fed is now clearly throwing the kitchen sink at the repo problem and failing, was today's increase in the overnight G/C repo rate which has once again started to rise ominously. Unfortunately, in its attempt to window-dress the issue, and pretend there is no problem at all, the Fed continues to pretend as if the problem isn't there, and following on this morning's comments from Lael Brainard that the repocalpyse was the result of a "simple imbalance" of supply and demand - and not a sign of deeper distress in credit markets - Dallas Fed president Kaplan said late on Wednesday that whereas the repo strain is important, it does not signal broader stress, and merely shows that the system needs more liquidity. To be sure, as we explained over the weekend, he is right about the latter, but wrong about the former, and to make it crystal clear to everyone that something is clearly broken with the systemic plumbing, here is repo market guru, Scott Skyrm, who works for Curvature Securities, and whose sole business is Repo financing in U.S. government securities, so yes, he knows better what he is talking about than any so-called fintwit expert. Let's just say that the Repo market is not so simple. Just a week ago I was singing praises to the Fed's overnight and term RP operations. Then, when rates backed-up the past two days, I was worried there was not enough cash in the system and the existing operations had failed. Now, it looks like smooth funding again! The Fed announced they are doubling the term and overnight RP operations tomorrow to $60 billion and $100 billion, respectively. When in doubt, throw more money at the problem! To be sure, if there is anything the Fed has demonstrated amply over the past decade, is that when in doubt, it will throw "enough money at the problem" that it will inflate the biggest asset bubble in history in the process. But it was Skyrm's punchline that was especially troubling as it confirms our worst fears: Now, here's the rub. It's great that the Fed is pumping liquidity into the system, however, why were the existing operations insufficient? As of today, the Fed had injected $105 billion in liquidity into the Repo market, but rates were still stubbornly high. Whatever changed last week to cause the funding spikes is clearly still an problem. Indeed it is, and unfortunately neither the Fed nor apparently anyone else, still has a clue what is going on. Which brings us to something else that Kaplan said late on Wednesday, namely that the Fed will now study what size the balance sheet should be in the future. Sound familiar? It should: that's precisely the exercise we conducted over the weekend, when we analyzed how much bigger the Fed's balance sheet will be in the coming year, and how the Fed will get there. For those who missed it: the Fed needs to boost its reserves by roughly $400 billion to get the total to $1.8 trillion. The only question is what how it will do it. And here we get to the bottom line, because whereas the Fed and its sycophantic media enablers are desperate to avoid calling the upcoming bond purchases by their real name, instead settling for the far more technical POMO, or permanent open markets operations, which as Goldman estimates will have to by roughly $15BN per month for a total of about $150BN per year... ... it was Bank of America that let it slip, and in a chart from BofAs' Michael Hartnett, the Chief Investment Strategist called what is coming by its real name: QE4. The problem, as Hartnett also identified, is that this will take the central banks' balance sheet to new all time highs, resulting in the biggest asset bubble in history getting even bigger... and setting up the world for an even greater crash when the fed's pushing on a string fails. And while nobody knows when that will happen, the fact that the financial system nearly collapsed last week even with $1.4 trillion in "excess" liquidity for reasons still unknown, means that like a great white shark, the market now needs constant liquidity injections, or else it will collapse. Finally, considering that it has now filtered down to even the average American that - courtesy of Bernie Sanders and Elizabeth Warren - that it is the Fed's market distorting operations that have resulted in a record wealth and income gap, we wonder: is it Trump's impeachment, or is it the Fed's upcoming QE4, that sets the stage for the now upcoming US civil war? The World's Wealthiest Families Are Stockpiling Cash as Recession Fears Grow

Suzanne Woolley and Ben Stupples BloombergSeptember 23, 2019 (Bloomberg) -- Rick Stone, a former partner at Cadwalader, Wickersham & Taft, sees treacherous times ahead for family offices trying to deploy cash. The head of Stone Family Office said he doubts the bond market will provide any real return over the next decade, that equity markets will suffer a substantial drop and then be flat, and that too much venture capital and private equity money will continue to chase too few opportunities. “It’s a very hard time for family offices to allocate money,” said Stone, 60, whose initial wealth came from class-action litigation fees. Stone has a good vantage point on the action, since he runs the bi-monthly meetings of the Palm Beach Investment Research Group, a network of 35 family offices in Palm Beach, Florida. “The areas to invest in are fewer, and there is a lot of money looking for those spaces,” he said. That view of the markets is shared by many of the 360 global single- and multi-family offices surveyed for the 2019 UBS Global Family Office Report, which was done in conjunction with Campden Research and released Monday. A majority expect the global economy to enter a recession by 2020, with the highest percentage of gloomy respondents in emerging markets. About 42% of family offices around the world are raising cash reserves. ‘More Caution’ “There’s more caution and fear of the public equity markets among ultra-high-net-worth investors,” said Timothy O’Hara, president of Rockefeller Global Family Office. “That has more people thinking about private investments, alternative investments or cash.” Jeffrey Gundlach, chief investment officer of DoubleLine Capital, said this month he thinks there’s a 75% chance of a U.S recession before the November 2020 presidential election, while economists surveyed by Bloomberg in August predicted a 35% chance in the next 12 months, up four percentage points from a month earlier. Meanwhile, the World Bank cut its 2019 global forecast to the slowest since the financial crisis a decade ago. Family offices have become a greater force in global financial markets. Campden estimates that such firms manage around $5.9 trillion. The offices in the UBS survey had an average of $917 million under management. Investing results have been mixed for those responding to the questionnaire, which was conducted between February and March. Average family-office returns for the 12 months prior to taking the survey were 5.4%, according to UBS. Developed-market equities were a big disappointment, providing an average 2.1% return. The highest average gains -- 6.2% -- were for family offices in the Asia-Pacific and emerging markets regions, followed by 5.9% in North America and 4.3% in Europe. Star Asset Private equity was the star asset class, with an average return of 16% for direct investments and 11% for funds-based investing. Real estate also performed well, returning an average 9.4%, and now makes up 17% of the average family-office portfolio, up 2.1 percentage points from last year’s survey. In the year ahead, 46% of families said they plan to put more money in direct private equity investments, with 42% devoting more to private equity funds and 34% funneling more into real estate, according to the survey. Family offices are also increasingly focused on a different kind of potential disruption: succession planning. This year, 54% of those surveyed said they have a succession plan in place, up from 43% last year. Just one-third of global family offices, however, said they have written plans. 28 Signs Of Economic Doom As Pivotal Month Of September Begins

ZeroHedge Tue, 09/03/2019 - 08:03 Authored by Michael Snyder via The Economic Collapse blog, Since the end of the last recession, the outlook for the U.S. economy has never been as dire as it is right now. Everywhere you look, economic red flags are popping up, and the mainstream media is suddenly full of stories about “the coming recession”. After several years of relative economic stability, things appear to be changing dramatically for the U.S. economy and the global economy as a whole. Over and over again, we are seeing things happen that we have not witnessed since the last recession, and many analysts expect our troubles to accelerate as we head into the final months of 2019. We should certainly hope that things will soon turn around, but at this point that does not appear likely. The following are 28 signs of economic doom as the pivotal month of September begins… #1 The U.S. and China just slapped painful new tariffs on one another, thus escalating the trade war to an entirely new level. #2 JPMorgan Chase is projecting that the trade war will cost “the average U.S. household” $1,000 per year. #3 Yield curve inversions have preceded every single U.S. recession since the 1950s, and the fact that it has happened again is one of the big reasons why Wall Street is freaking out so much lately. #4 We just witnessed the largest decline in U.S. consumer sentiment in 7 years. #5 Mortgage defaults are rising at the fastest pace that we have seen since the last financial crisis. #6 Sales of luxury homes valued at $1.5 million or higher were down five percent during the second quarter of 2019. #7 The U.S. manufacturing sector has contracted for the very first time since September 2009. #8 The Cass Freight Index has been falling for a number of months. According to CNBC, it fell “5.9% in July, following a 5.3% decline in June and a 6% drop in May.” #9 Gross private domestic investment in the United States was down 5.5 percentduring the second quarter of 2019. #10 Crude oil processing at U.S. refiners has fallen by the most that we have seen since the last recession. #11 The price of copper often gives us a clear indication of where the economy is heading, and it is now down 13 percent over the last six months. #12 When it looks like an economic crisis is coming, investors often flock to precious metals. So it is very interesting to note that the price of gold is up more than 20 percent since May. #13 Women’s clothing retailer Forever 21 “is reportedly close to filing for bankruptcy protection”. #14 We just learned that Sears and Kmart will close “nearly 100 additional stores”by the end of this year. #15 Domestic shipments of RVs have fallen an astounding 20 percent so far in 2019. #16 The Labor Department has admitted that the U.S. economy actually has 501,000 less jobs than they previously thought. #17 S&P 500 earnings per share estimates have been steadily falling all year long. #18 Morgan Stanley says that the possibility that we will see a global recession “is high and rising”. #19 Global trade fell 1.4 percent in June from a year earlier, and that was the biggest drop that we have seen since the last recession. #20 The German economy contracted during the second quarter, and the German central bank “is predicting the third quarter will also post a decline”. #21 According to CNBC, the S&P 500 “just sent a screaming sell signal” to U.S. investors. #22 Masanari Takada is warning that we could soon see a “Lehman-like” plunge in the stock market. #23 Corporate insiders are dumping stocks at a pace that we haven’t seen in more than a decade. #24 Apple CEO Tim Cook has been dumping millions of dollars worth of Apple stock. #25 Instead of pumping his company’s funds into the stock market, Warren Buffett has decided to hoard 122 billion dollars in cash. This appears to be a clear indication that he believes that a crisis is coming. #26 Investors are selling their shares in emerging markets funds at a pace that we have never seen before. #27 The Economic Policy Uncertainty Index hit the highest level that we have ever seen in the month of June. #28 Americans are searching Google for the term “recession” more frequently than we have seen at any time since 2009. The signs are very clear, but unfortunately we live at a time when “normalcy bias” is rampant in our society. If you are not familiar with “normalcy bias”, the following is how Wikipedia defines it… The normalcy bias, or normality bias, is a belief people hold when considering the possibility of a disaster. It causes people to underestimate both the likelihood of a disaster and its possible effects, because people believe that things will always function the way things normally have functioned. This may result in situations where people fail to adequately prepare themselves for disasters, and on a larger scale, the failure of governments to include the populace in its disaster preparations. About 70% of people reportedly display normalcy bias in disasters.[1] For most Americans, the crisis of 2008 and 2009 is now a distant memory, and the vast majority of the population seems confident that brighter days are ahead even if we must weather a short-term economic recession first. As a result, most people are not preparing for a major economic crisis, and that makes us extremely vulnerable. In 2008 and 2009, the horrible financial crisis and the bitter recession that followed took most Americans completely by surprise. It will be the same this time around, even though the warning signs are there for all to see. |

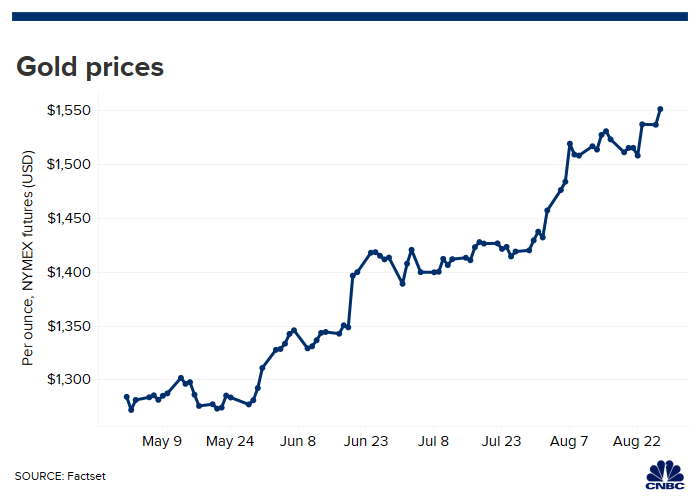

Archives

December 2020

Categories |

RSS Feed

RSS Feed

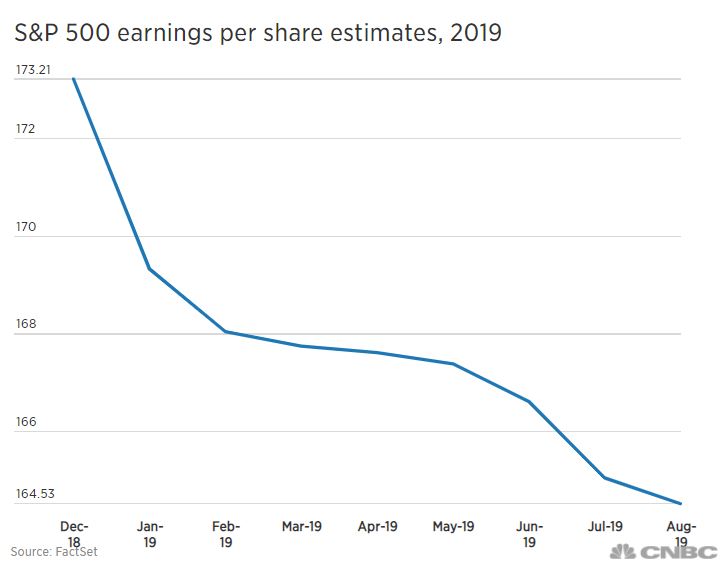

{kind=link}

{kind=link}

{kind=link}

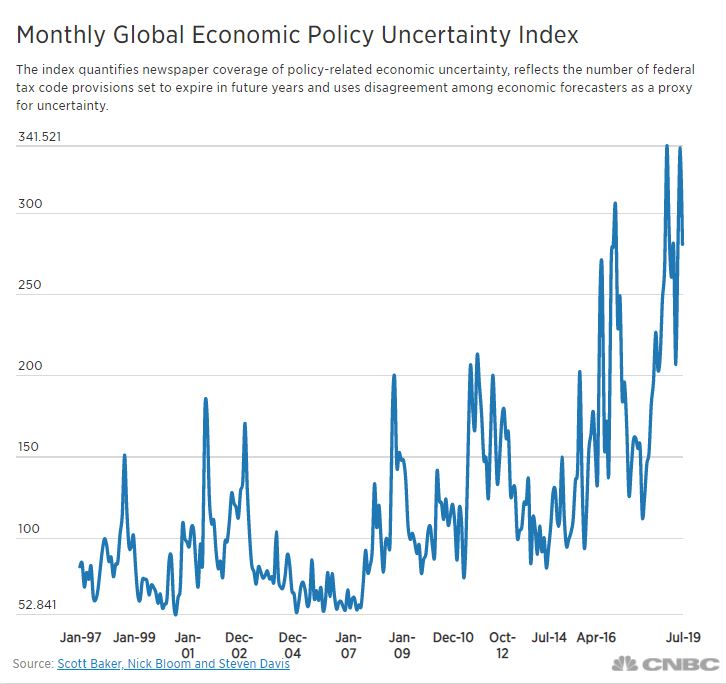

{kind=link}